This observe addresses these points utilizing knowledge for Alphabet, an organization that could be a poster baby for development alternatives and investing in intangible property.

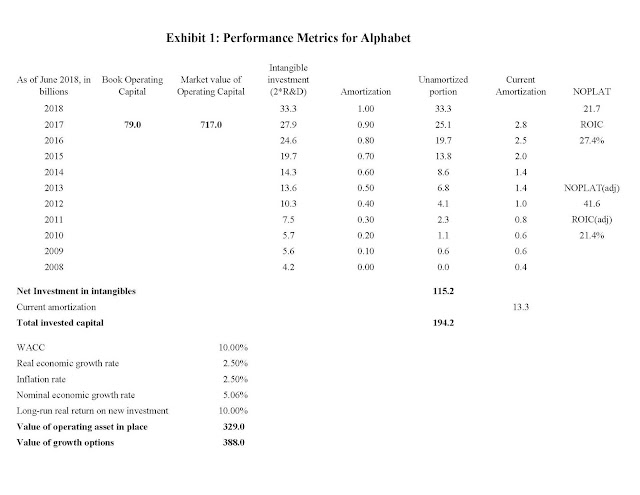

Third, when each NOPLAT and invested capital are adjusted to account for intangibles, ROIC(adj) falls to 21.4%. The adjustment for NOPLAT consists of reversing bills for intangible property and deducting depreciation on intangible property. For Alphabet, the impression of including funding in intangibles to the denominator outweighs the impression of including internet funding spending again to the numerator.

There are two explanations for the massive distinction between the e-book worth of invested capital, together with intangible property, and the market worth. The primary is that Alphabet’s investments in each tangible and intangible property are constructive internet current worth (NPV) initiatives at inception. If an funding is constructive NPV, as quickly because the asset is put in place, its market worth exceeds the capital invested. This raises the query of the place the constructive NPV initiatives come from. In a aggressive market they might not exist. The reply should be that they will primarily be attributed to the already present intangible capital – one thing that competing firms can’t copy. It’s by combining the brand new investments with the already present intangible property that constructive NPV initiatives are created. Some may say: what if the corporate merely scans the markets extra fastidiously and thereby finds constructive NPV initiatives? However the skill to do such scouring is a type of intangible capital. So, as soon as once more, present intangible property are the supply of worth creation. Second, over time, the market frequently re-evaluates the worth of working capital property, together with intangible property, primarily based on the money flows they’re anticipated to supply.

Such revaluations can widen the hole between the quantity invested in intangible property and their market worth.

Turning to development alternatives, as initially outlined by Myers (1977), development alternatives or development alternatives are “finest seen as the current worth of the corporate’s skill to make future investments. The excellence drawn right here is between property whose final worth is dependent upon extra discretionary funding by the enterprise and property whose final worth doesn’t rely on such funding..” Myers then divides the overall worth of the corporate into two elements: the worth of the property in place and the worth of the expansion alternatives. He would not attempt to describe how any of them needs to be calculated for an precise firm like Alphabet.

Earlier than addressing the valuation of development alternatives, there’s a preliminary query concerning the relationship between intangible property and development alternatives. Contemplate two firms, one in all which has helpful development alternatives and the opposite of which doesn’t at present differ in a roundabout way that explains the existence of the expansion alternatives. This distinction might be a type of intangible capital. Admittedly, it may be troublesome to determine precisely which intangible property present the expansion alternatives for one firm and never the opposite.

For instance, development alternatives could also be associated to extra nebulous intangibles, similar to the corporate’s organizational construction or worker expertise, however whatever the exact supply, development alternatives should be associated to some intangible property that an organization possesses however others don’t. This means that if intangible capital is outlined with enough generality, there are not any extra development alternatives. The corporate’s market worth corresponds to the market worth of the working property broadly outlined. The explanation for emphasizing what could look like a pedantic distinction is to keep away from double counting. If all intangibles are totally accounted for, there isn’t any want so as to add development alternatives. Put one other means, the worth of the corporate will be considered equal to the worth of property in place plus the worth of the expansion alternatives or the worth of tangible plus intangible property, however the two shouldn’t be blended.

The above doesn’t indicate {that a} division of the working market worth into the worth of development alternatives and the worth of the property in place is nugatory, it merely implies that it relies upon totally on the definition of “property in place.” If property in place are broadly outlined to incorporate all intangible property of any kind, then the worth of the expansion alternatives is zero. However that is not a means property in place are usually outlined. A extra widespread definition is to say that the worth of the property in place is the same as the working worth of the corporate, assuming that from the present date it solely grows consistent with the general financial system. By way of valuation modeling, that is equal to assuming that the present NOPLAT represents the “terminal 12 months” and assuming regular development thereafter. In Appendix 1, I assumed secure development of 5.06% primarily based on each inflation and actual development equivalent to 2.5%. I additionally assume that real the return on new funding in regular state is 10.0%. Given these assumptions, the terminal worth (which by assumption is the same as the worth of the property in place) will be calculated utilizing the plowback formulation described by Bradley and Jarrell (2008) and Cornell and Gerger (2017). The consequence, as proven in Exhibit 1, is that the worth of property in place involves $329 billion, leaving $388 billion as the worth for development alternatives. Be aware that the worth of the property in place exceeds the invested capital, together with intangible property, of $194 billion. This is smart as a result of the intangible property not solely produce the expansion alternatives, but in addition improve the present incomes energy of the invested capital, which is mirrored in the truth that the ROIC exceeds the WACC. It’s after all attainable to outline the property in place in another way.

For instance, consulting agency Charles River Associates makes use of 5 years of analyst forecasts to forecast NOPLAT for the following 5 years and assumes regular development thereafter. For Alphabet, the applying of this process will increase the estimated worth of the property in place and correspondingly reduces the worth of the expansion alternatives. This emphasizes the important thing level that development alternatives are a residual whose worth is dependent upon the process used to calculate the worth of property in place.

Working capital is outlined minus money and short-term investments.