Macro letter – no. 135 – 31-12-2020

US shares in 2020 and the outlook for 2021

- 2020 has been a violent yr for inventory markets globally

- Fiscal and financial stimulus rescued buyers from a brutal bear market

- Digital transformation has accelerated and the fortunes of the expertise sector with it

- With mass vaccination nonetheless a way off, 2021 will see many tendencies proceed

The US inventory market reaches file highs (as at 29th December). It has been a violent yr. The 35% shakeout within the S&P 500 seen in March turned out to be the most effective shopping for alternative in years. The market recovered regardless of the human tragedy of the pandemic, fueled by a cocktail of financial and monetary stimulus. When information of the rollout of a vaccine lastly got here in November, other than a renewed rally within the broad market, there was an abrupt rotation from progress to worth shares. Worth ETFs noticed $8 billion. inflows in November, there was additionally a weakening of the US$ and the resurgence of European shares. This was not essentially the case sea change assumed by many commentators by early December, expertise shares had resumed their upward march.

November marked some market data. It was the strongest month for the Dow since 1987 and the most effective November since 1928. European shares rose 14%, their greatest month-to-month achieve since April 2009 – to qualify the headlines, European indexes stay decrease than they began the yr. For Japan’s Nikkei 255, the 15% achieve marked its most constructive month-to-month efficiency since January 1994, whereas for World Equities, which returned 12.7%, it was the most effective month since January 1975.

Different monetary and commodity markets additionally reacted to the vaccine information. OPEC agreed provide cuts which are serving to oil costs rise, though Brent Crude stays about 22% decrease than it began the yr. The larger concern for the inventory markets is the logistical problem of delivering the vaccination, this may take a look at the well being methods of each nation on the planet. The OPEC settlement might fray on the edges, the demand for oil might come later than anticipated. However, threat belongings have typically benefited, whereas each gold and silver have remained range-bound. After their robust summer season rally, treasured metals seem to have had their time within the solar. Apparently, Bitcoin appears to be dancing to a unique tune. Over the previous two months, it has risen greater than 120%, breaking the earlier highs of December 2017 and reaching $28,000.

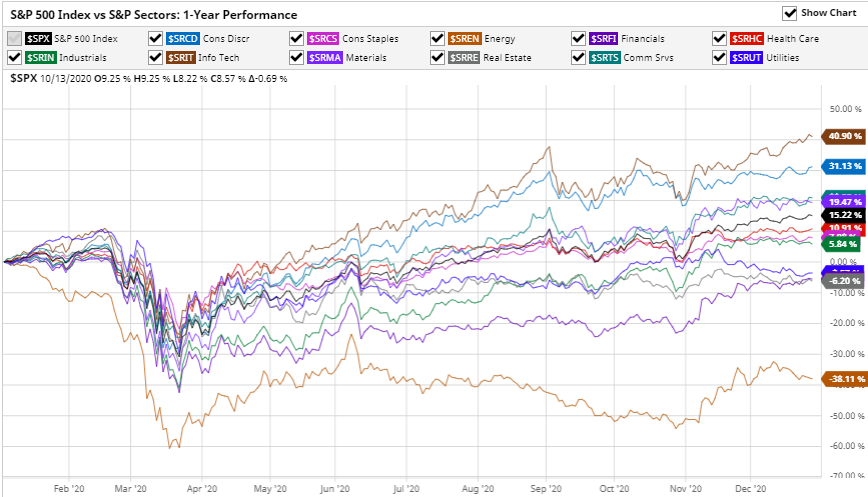

Wanting forward, Covid-sensitive shares ought to proceed to get well, this chart exhibits the relative efficiency per industrial sector over the past yr (to 29th December): –

Supply: Barchart.com, S&P

Power, November’s best-performing sector, continues to be down greater than 38% over the previous 12 months, whereas info expertise is up practically 41% over the identical interval.

Outlook for 2021

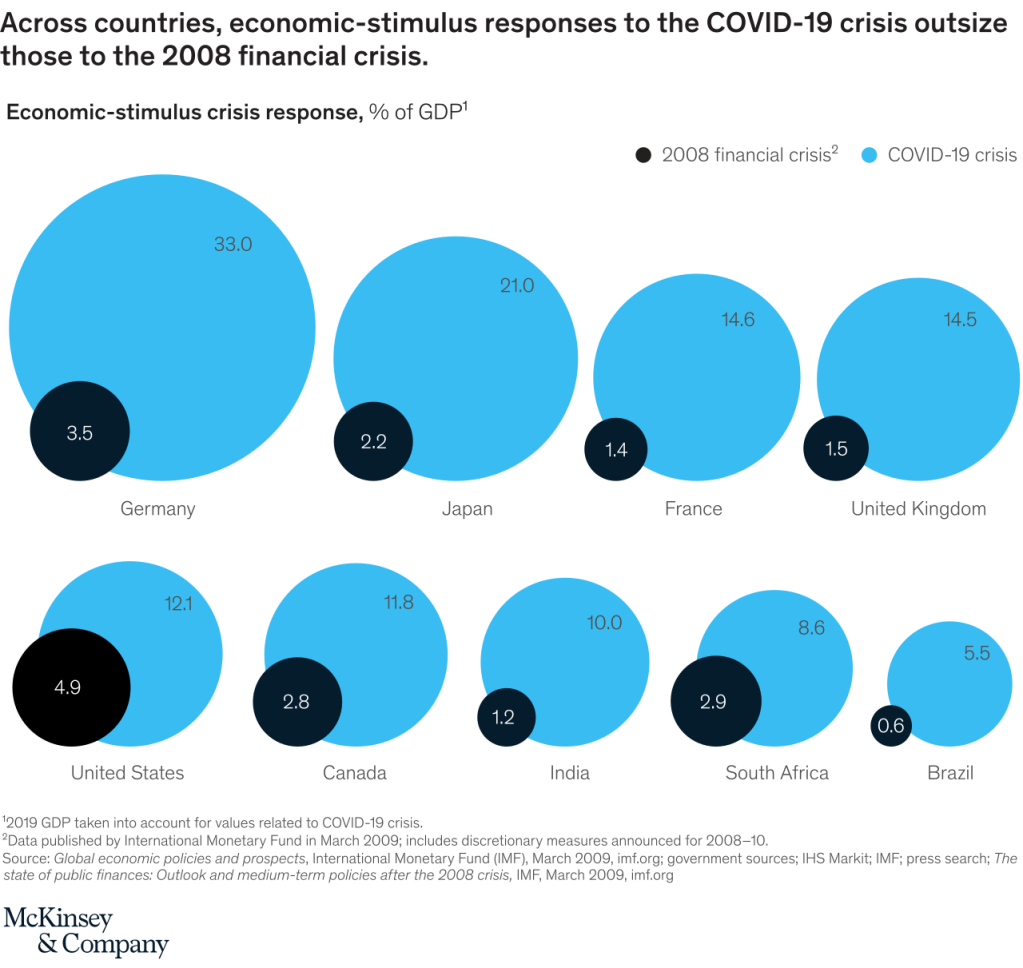

The financial coverage of central banks and the fiscal coverage of developed international locations will likely be key in figuring out the course of shares subsequent yr. This infographic from McKinsey exhibits the large scale of the fiscal response in comparison with the Nice Monetary Disaster of 2008:-

Supply: McKinsey, IMF

The diploma of largesse should be certified, greater than half of the general public help has been within the type of ensures, designed to assist corporations keep away from insolvency. As well as, different stimulus measures have been introduced, however the capital has not but been allotted. The ultimate invoice for the pandemic is probably not fairly the pressure on collective worldwide sovereign funds that the McKinsey infographic portends. This chart from the IMF exhibits the composition of fiscal help in mid-Might: –

Supply: IMF

A extra vital issue for world equities is the large injection of liquidity that has been pumped into the world economic system: –

Supply: Yardeni

This world image hides the distinction between the international locations: –

Supply: Federal Reserve, Nationwide Central Banks, Haver Analytics, Globalization Institute

Excluding the US, cash provide progress has been comparatively subdued up to now, though broadly corresponding to the enlargement within the wake of the sub-prime disaster in 2008. The large enlargement of the US financial base is unprecedented by comparability with its developed friends nations, however much more so when considered within the context of US coverage since World Struggle II:-

Supply: Gavekal/Macrobond

Cash provide progress can’t be ignored when on the lookout for a motive for the rise in US shares. North American asset markets, reminiscent of shares and actual property, will proceed to profit, at the same time as a few of that liquidity trickles away to worldwide funding alternatives. The Cantillon impact, named after the 18th-century Irish economist Richard Cantillon, continues to be going robust. IN Cantillon’s – Essay on the Nature of Commerce in Basic – which was revealed posthumously in 1755 – he noticed that these closest to the minting of cash benefited most.

Immediately, with unemployment considerably greater and lockdown restrictions limiting consumption, the American financial savings charge has risen considerably. Even after peaking in April, it stays nicely above ranges seen for the reason that Seventies. The chart beneath doesn’t bear in mind the impact of the newest aid bundle, which is able to launch a further 900 billion. USD together with checks to many people of USD 600 every: –

Supply: Federal Reserve Financial institution of St. Louis

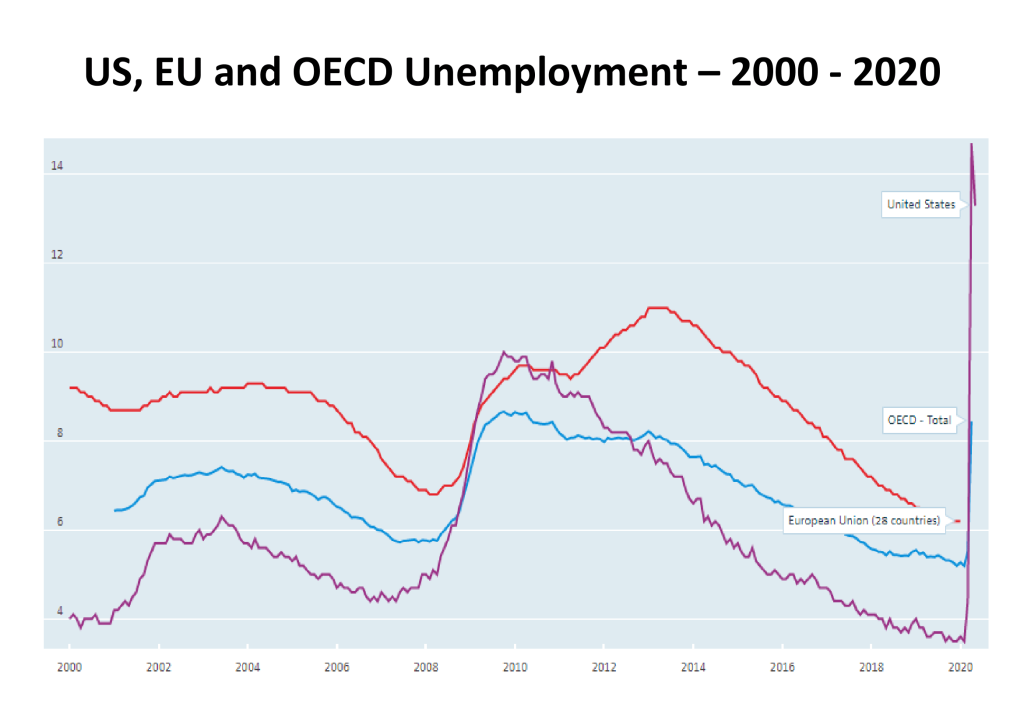

Whereas unemployment stays excessive, the surplus liquidity will both be hoarded or move into the inventory market, in these unsure instances it’s unlikely to spark a spending increase. This chart exhibits how general unemployment has elevated within the US, EU and OECD international locations: –

Supply: OECD

Aside from a short-lived increase within the grocery sector at the start of the disaster, US consumption remained subdued through the summer season: –

Supply: NEBR

The scenario improved within the third quarter, because the infographic beneath reveals: –

Supply: Deloitte, BEA, Haver Analytics

Actual personal consumption elevated by 8.9% within the third quarter in comparison with the 2nd quarter. The character of shopper spending has additionally modified on account of the pandemic, with many customers shopping for comparatively extra items than providers. With out dependable knowledge, it’s troublesome to evaluate the image for This fall, however the second wave of Corona instances appears to be a worldwide phenomenon, a repeat of the April/Might lockdown might but delay the long-awaited restoration in consumption.

Funding alternatives for 2021

Wanting forward, the primary vital take a look at of American political sentiment would be the Senate race in Georgia on January 5.th. However, within the yr forward, with authorities bond yields nonetheless miserably low, extra liquidity will proceed to move into shares. The latest weakening of the US$ might present additional help to worldwide markets, particularly if Europe stops its bickering and embraces fiscal enlargement. Greenback bulls may be saved by the US bond market, 10-year yields hit 99bps in early December, the best for the reason that pandemic hit in March, rates of interest have remained excessive with a brand new funding stimulus bundle, however an financial restoration continues to be a way off manner off, an actual bond carry market wants a big inflationary catalyst.

As Milton Friedman famously noticed: ‘Inflation is all the time and in all places a financial phenomenon.’ Even permitting for a robust restoration in demand for items and providers in 2021, the buyer will stay cautious till mass vaccination is confirmed to be efficient. Within the meantime, the surplus liquidity has to go someplace, different issues being equal, asset markets will rise with liquid, listed shares main the best way.