The financial institution failures of Silicon Valley Financial institution and Signature Financial institution had been important financial occasions. These failed banks had been taken over by the FDIC on March 10th and 12th, respectively. Regulators labored to calm the market on March 12th by issuing an announcement that the banking system “stays strong and on a strong basis.”

To essentially perceive what is going on on, let’s look at the financial institution information instantly. The just lately printed figures now permit a take a look at how the banks are literally dealing with the state of affairs. This makes it attainable to evaluate the remaining degree of stress within the banking sector.

Direct loans from the Fed recommend that the chance of financial institution failure has not been resolved

Main as much as and thru the financial institution crashes, one would count on the banks to lend more cash. However when the disaster was over and the insurances got by the authorities, there can be no want for the banks to lend much more cash.

Loans not solely elevated, however elevated greater than the week the failures occurred. Banks pay curiosity on borrowed funds and wouldn’t lend cash with out motive. It is sensible for a financial institution to borrow if it could actually make investments the cash at a price that’s greater than the price of borrowing. That is unlikely to be the case within the present rate of interest surroundings. Due to the Fed’s price hikes, the price of borrowing exceeds the return on secure investments.

The opposite motive a financial institution would borrow is that if it wanted to lift money to fulfill depositor demand. That is extra possible what occurs.

An affordable possibility is for depositors in sure banks to withdraw or just use their accounts. This in flip might result in some banks being required to lend to offer depositors entry to their funds.

Borrowing cash from the Fed eliminates the necessity for banks to promote their bonds. This can be a handy resolution as a result of the banks shouldn’t have to acknowledge losses on their bonds beneath face worth. Nonetheless, the financial institution should additionally pay curiosity on borrowed funds. It will minimize into their profitability.

Financial background

The above information is direct proof of economic stress within the banking sector. However protecting your entire financial and regulatory surroundings in thoughts will assist to supply the clearest attainable image.

The failures of Silicon Valley Financial institution, Signature Financial institution and Credit score Suisse destroyed important wealth. Tens of billions of {dollars} in shares and bonds had been wiped off the market. The fallout from this destruction of wealth might not have trickled by means of the financial system but. Will this power a few of their buyers to liquidate a part of their financial institution accounts to cowl funds? Or may one other financial institution have misplaced sufficient holding inventory or bonds in these failed banks that writing them off would additionally make it bancrupt? These are tough inquiries to know for positive, however it is extremely attainable that there may very well be lasting results.

Regulatory background

Modifications made by the Federal Reserve imply that banks now not want reserves to fulfill regulatory necessities. The Fed refers to this as an ample reserve regime. What this really means is that there isn’t any longer a requirement for a financial institution to carry any a part of your deposits in money or on deposit on the nearest Fed department. This enables banks to speculate as much as 100% of your deposits. If their investments fall, there isn’t any liquid buffer beneath the Ample Reserve Regime to supply for depositor funds. Likewise, if extra folks use or withdraw their cash than the financial institution anticipated, the financial institution will run wanting money.

The Federal Reserve eliminates the requirement that banks maintain reserves, ushering in a brand new period of banking regulation in the USA. This experiment has solely been in place since March 26, 2020. Till very just lately, the banking system had been comparatively liquid with money. In response to the 2008 crash and the coronavirus, the Fed pumped out new cash. This cash discovered its manner into the banking system. Now that the Fed has began to take away cash, we might discover that no less than some banks didn’t have ample reserves and are in hassle.

Threat of financial institution failure – kickers

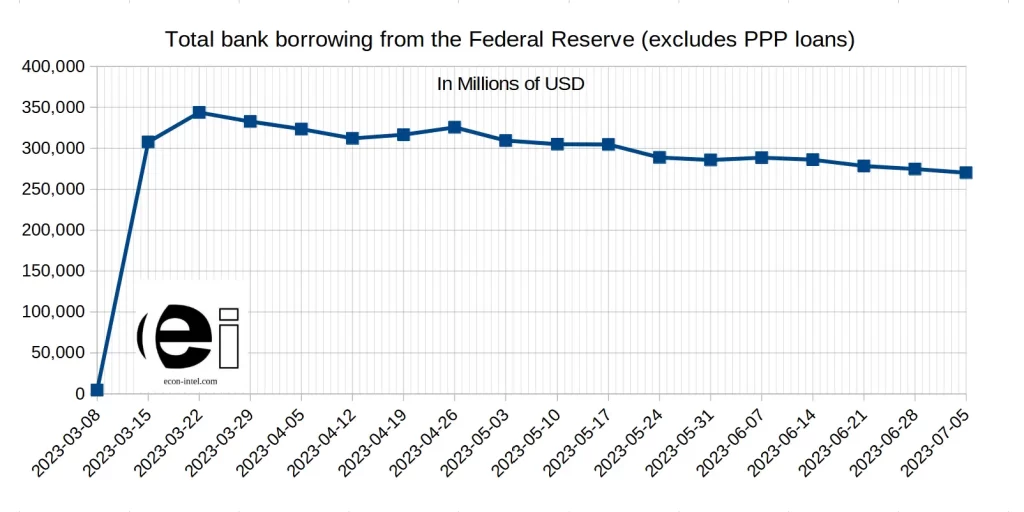

The $330 billion that banks borrow from the Federal Reserve is lower than the document for borrowing from the Fed. This document was set within the week ending October 15, 2008 at almost $438 billion. Nonetheless, there’s a large distinction in what these numbers measure. It isn’t an apples to apples comparability. In 2008, laws required banks to carry reserves. If their reserves fell beneath the reserve requirement, they may borrow the distinction from one other financial institution or the Federal Reserve. Which means that banks borrowed to fulfill their reserve necessities. In different phrases, the borrowing meant that the financial institution had issues sustaining the reserve degree. Not that it was out of money.

Right this moment there isn’t any reserve requirement. So banks don’t have to lend till they want instant funds. True, a financial institution may borrow to make investments or borrow to keep away from promoting a safety at a loss. However as talked about above, the likelihood of borrowing for funding is low. That is very true given the excessive ranges of borrowing we’re presently seeing. Moreover, if historical past serves as a information, banks borrow little or no from the Fed besides in instances of disaster.

In 2008, it wasn’t simply the banks that lent

Moreover, the $330 billion of borrowed funds at the moment represents all financial institution borrowing. The 438 billion {dollars} represented loans to banks, cash market funds and different monetary establishments. So whereas the quantity in 2008 was bigger, it was not greater solely inside the banking sector.

It’s too early to conclude that the banking disaster is over. We’ll see how the assurances of a “wholesome and strong” banking sector age. Maybe no higher than the time period “transient inflation” has.

Till Fed lending to banks declines, there are more likely to be financial institution liquidity considerations lurking behind the scenes.

Replace on 3/31/23: Information launched yesterday point out that Federal Reserve financial institution loans (excluding PPP loans) fell about $11 billion from near $344 billion on March twenty second to roughly $333 billion on March twenty eighth. This can be a constructive signal that banking stress could also be easing. Nonetheless, the banks’ borrowing from the Fed continues to be considerably greater.

Replace on 5/12/23: Whereas Federal Reserve lending to banks has declined from their peak, the change continues to be minimal. We warned within the unique article, shortly after Silicon Valley Financial institution failed, that we had been skeptical concerning the soundness of the banking sector. Since then, a good bigger financial institution, First Republic, has failed. At current, we nonetheless see little motive to imagine that the monetary stability of the banking system has considerably improved.

Listed below are financial institution loans from the Fed (excluding OPP loans):

Replace on 6/5/23: At current, there may be nonetheless little motive to imagine that the banking system has recovered and stabilized. To assist folks higher shield themselves towards financial institution failures, we have compiled financial institution security reviews for every FDIC-insured financial institution. Discover the reply to the query “Is my financial institution secure?”

Replace on 7/7/23: At this level, it seems that the downward development in financial institution borrowing from the Fed has been established for an extended sufficient interval that one may fairly imagine that the banking disaster is resolving. That mentioned, the extremely sluggish tempo returning to baseline is clear. This leaves little doubt that important stress stays in no less than a number of the banks. This additionally implies {that a} important shock to the trade may reignite the financial institution failure disaster.

Observe us right here:

Source link