Macro letter – no. 138 – 21-05-2021

First in, first out – China as a number one indicator

- China was the primary nation to get better from the Covid-19 pandemic

- The PBoC started tightening financial situations in Might 2020

- Chinese language housing and shares stay sturdy regardless of official coverage

- Chinese language contagion stays a threat to the worldwide restoration

Whereas there are a lot of facets of the Chinese language command financial system which differs radically from that of the US, it’s price analyzing the efficiency of China’s financial system, fiscal and financial coverage, and its monetary markets. They’ll present some perception into the long run course for different developed and growing markets as we progressively emerge from the Covid disaster:-

Supply: Commerce financial system

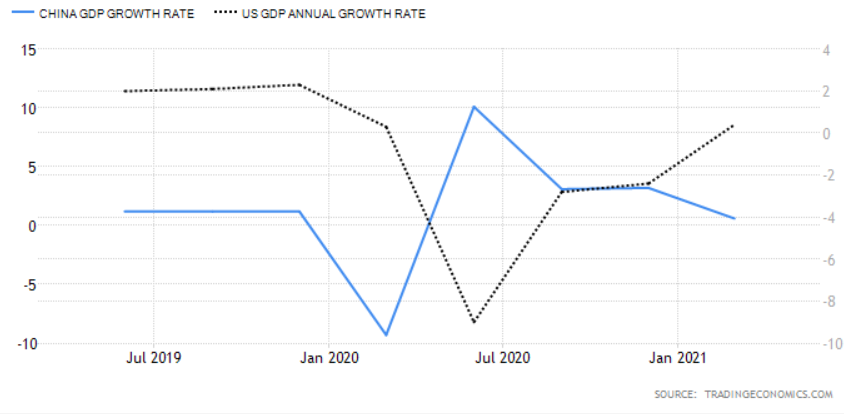

As will be seen from the chart above, China was the primary nation to be hit by the Covid-19 pandemic, but it surely was additionally the primary nation to get better, however a comparability of the Chinese language and US bond markets paints a considerably completely different image : –

Supply: Commerce financial system

Chinese language bond yields hit their lowest ranges across the identical time because the US, since then they’ve returned extra rapidly to their pre-pandemic ranges. If the US follows an identical trajectory, the rate of interest on US authorities bonds will rise additional.

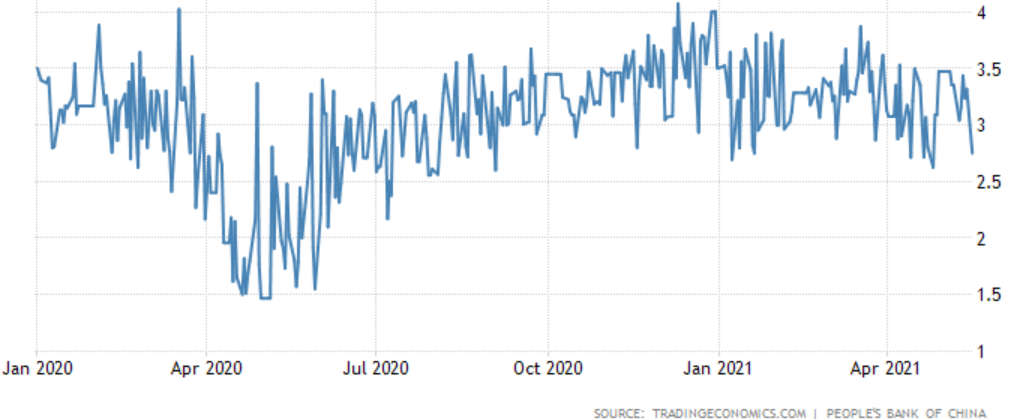

Nevertheless, it may be argued that the state of affairs within the Chinese language bond market is a perform of the financial stance of the Folks’s Financial institution of China (PBoC). When the disaster first erupted, the PBoC lower its rate of interest hall by 0.3% and in addition lowered Chinese language interbank charges by round 1.2% by means of its open market operations. By Might 2020, this coverage had modified, housing changed by a relentless drain of liquidity.

The chart beneath exhibits the reasonably unstable 3-month Shibor charge, that is in marked distinction to the ‘decrease for longer’ method following the 2008 disaster. The Covid lodging has been remarkably short-lived:-

Supply: Buying and selling Economics, PBoC

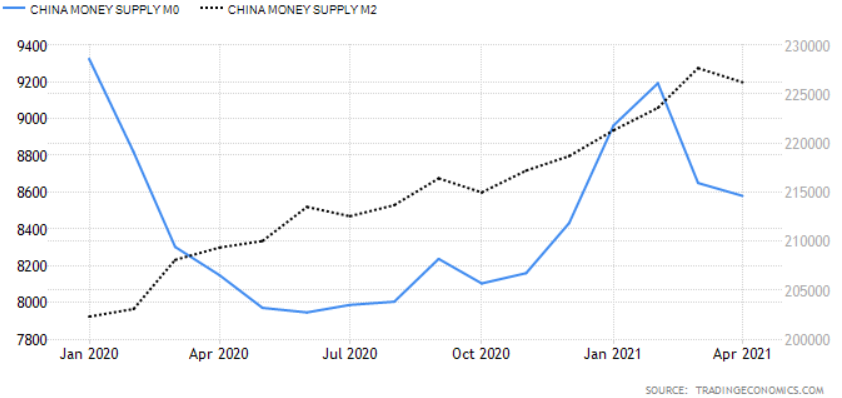

This PBoC tightening, which started in Might 2020 and has been accompanied by official discuss in regards to the want for stability and the need to keep away from creating asset bubbles, is lastly turning into evident within the cash provide knowledge: –

Supply: Commerce financial system

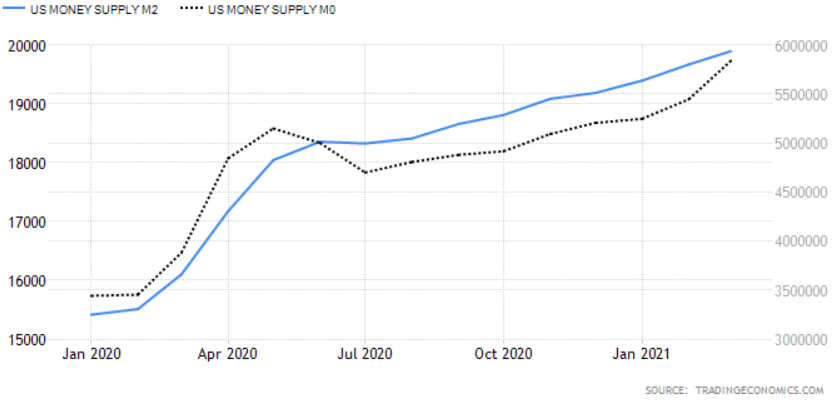

This contrasts with the continued growth of US cash provide: –

Supply: Commerce financial system

One of many challenges dealing with all central bankers is that rates of interest are a blunt software. Not all of China’s asset markets have heeded the PBoC recommendation. The residential property market stays, for instance, crimson scorching regardless of the introduction of three crimson traces coverage – which goals to restrict their liabilities-to-assets ratio (excluding advance revenue) to lower than 70%, or their web gearing to lower than 100%, or their cash-to-current debt ratio to lower than 1x, or a mix of all three. New residence costs rose regardless, rising 4.8% in April, led by luxurious properties in Shenzhen, Shanghai and Guangzhou, which have risen 16% to 19% over the previous yr – additional tightening of regulation appears inevitable.

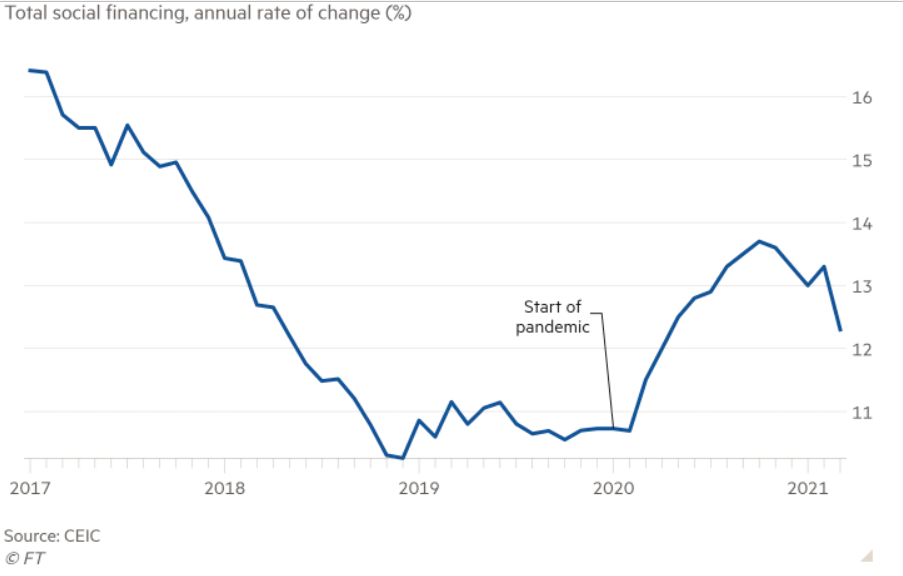

The PBoC has been extra influential elsewhere, Complete Social Financing, their most popular measure of lending throughout your entire home monetary system, rose 12% in March, the slowest tempo since April 2020:-

Supply: Monetary Instances, CEIC

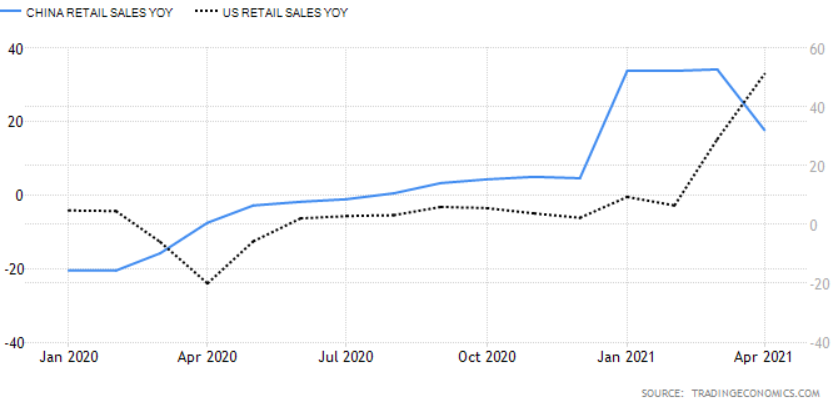

One other signal that official coverage motion could also be biting was seen in April retail gross sales, which, whereas rising 17.7%, fell from 34.2% in March and got here in properly beneath the consensus forecast of 24.9%. Right here too, China seems to be a number one indicator of the course the US financial system might take: –

Supply: Commerce financial system

Curiously, in contrast to 2015, the Chinese language inventory market has to date reacted extra measuredly to the overall tightening of financial situations. The subsequent chart exhibits the relative efficiency of the Shanghai Composite towards the S&P 500 index: –

Supply: Commerce financial system

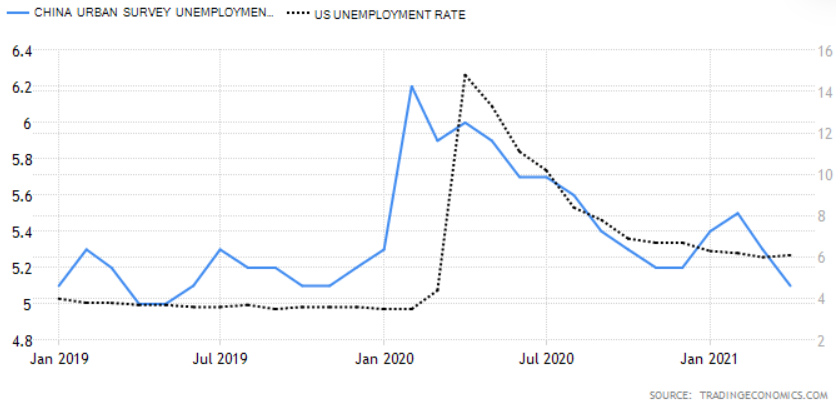

As talked about above, cash provide knowledge factors to a slowdown within the Chinese language financial system, however like so many different international locations, China skilled a pointy improve in its already excessive family financial savings. The Paulson Institute estimates that Chinese language households saved 3% extra of their revenue than earlier than Covid; Pantheon Macroeconomics equates this pool of financial savings to round 3% of GDP. Whereas many commentators counsel that in China’s case it is a pool of preventive financial savings, consumption is more likely to resume its long-term progress now that employment prospects have begun to enhance. The chart beneath exhibits the lagged unemployment trajectory within the US in comparison with China:-

Supply: Commerce financial system

US unemployment stays excessive relative to its pre-Covid charge, however the financial restoration continues to achieve momentum.

In China, as elsewhere, the portion of extra financial savings that’s not consumed will both be left on deposit, used to scale back debt, or invested. Though rates of interest have risen, liquidity in Chinese language capital markets ought to stay ample for the subsequent six months to a yr, ample to cushion any sudden downturns within the post-Covid restoration.

Conclusions and funding alternatives

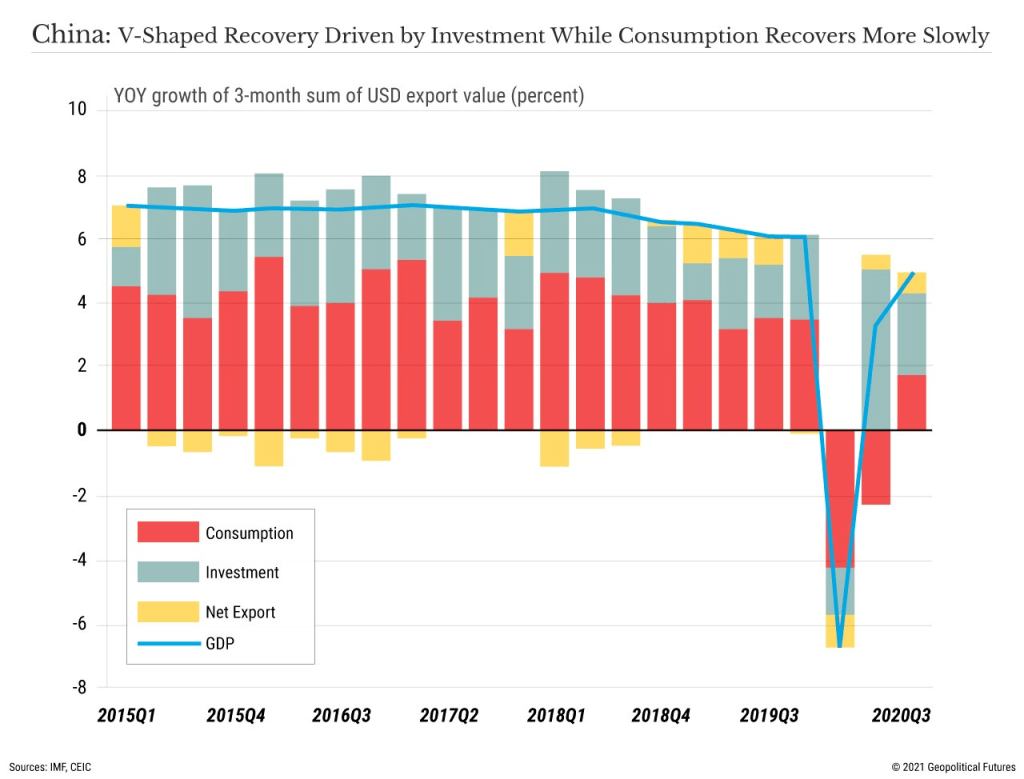

Within the evaluation above, I’ve created a sequence of charts that counsel the US might observe China’s path because the post-Covid restoration unfolds. That is virtually actually too easy. Above all, Beijing craves stability, it is aware of that the tempo of financial progress is slowing, it’s structural. The investment-led progress mannequin that has reworked the financial system over the previous 4 many years requires methadone of extra credit score to maintain even these decrease returns. The coverage of rebalancing in the direction of home consumption gives hope in the long term, however China’s restoration from the Covid disaster was primarily pushed by funding and to a a lot lesser extent exports. The chart beneath, from George Friedman of Geopolitical futureexhibits the injury to Chinese language consumption from the pandemic and the following restoration:-

Supply: Geopolitical Futures, IMF, CEIC

The brand new(ish) US administration can also be completely different than the one we have seen in many years. The markets imagine within the arrival of a New New Deal pushed by a huge financial and monetary tonic which can heal all. Asset costs proceed to rise as The the whole lot bubble inflated additional.

We’re nonetheless within the early phases of the financial restoration. Provide chain constraints and labor shortages, though underemployment stays excessive, have pushed inflation expectations greater within the close to time period, but asset markets look past these short-term components to the productiveness positive aspects that in lots of instances have been a long-awaited response to the disaster itself.

Just a few courageous central bankers want to curb the hypothesis frenzy. Nevertheless, the bulk will put their weight on outcomes reasonably than prospectsas Federal Reserve Governor Lael Brainard not too long ago acknowledged. This politically expedient method implies that fiat currencies will proceed their race to the underside, bond markets will stay sterilized by QE coverage; that leaves property just like the solitary security valve someplace in between a storehouse of wealth and thar she blows. They supply some safety towards degradation and, with the arrival of Decentralized financial system, there’s a non-zero risk that a few of these property might even develop into a medium of change.

Within the brief time period, we have now seen Norges Financial institution point out that it might elevate rates of interest within the second half of 2021. The Financial institution of Canada has introduced a tapering of presidency bond purchases, underscoring a possible charge hike in late 2022, whereas the Financial institution of Japan, whereas it has not made bald statements, has moderated its ETF purchases and is being accused of taper by stealth as a result of the quantity of its bond purchases has really slowed because it was enacted administration of the yield curve in 2016. These remoted actions are simply clouds in a blue sky of infinite liquidity, however monetary markets favor to journey reasonably than arrive. Bigger markets are probably over the subsequent few months and there could also be some glorious alternatives to purchase property on sharp corrections.