Macro letter – No. 139 – 18-06-2021

Uncooked supplies, provide chains and structural adjustments in demand

- Discuss of a brand new commodity supercycle could also be untimely

- As soon as GDP progress returns to development, commodity demand will average

- Fiscal and financial reduction is essential to sustaining progress and demand

- Structural adjustments in vitality demand will show extra persistent

Because the specter of inflation begins to hang-out economists, many market commentators have begun to concentrate on commodity costs in an try and predict the probably path of the overall value stage for items and companies. This indexing of probably the most heterogeneous asset class has at all times struck me as doomed to disappoint. Commodity costs change in response to, usually, small variations in provide or demand, and the value of some commodities varies enormously from one geographic location to a different. Often, most gadgets rise in time, however extra usually they dance to their very own distinctive tunes.

Commodity analysts are inclined to focus totally on vitality and industrial metals; Agricultural commodities, that are extra numerous in nature, are sometimes left as a footnote. Often, nevertheless, a demand-side occasion happens that causes nearly all sectors to rise. The Covid-19 occasion was simply such a shock, disrupting international provide chains and shopper demand patterns on the similar time.

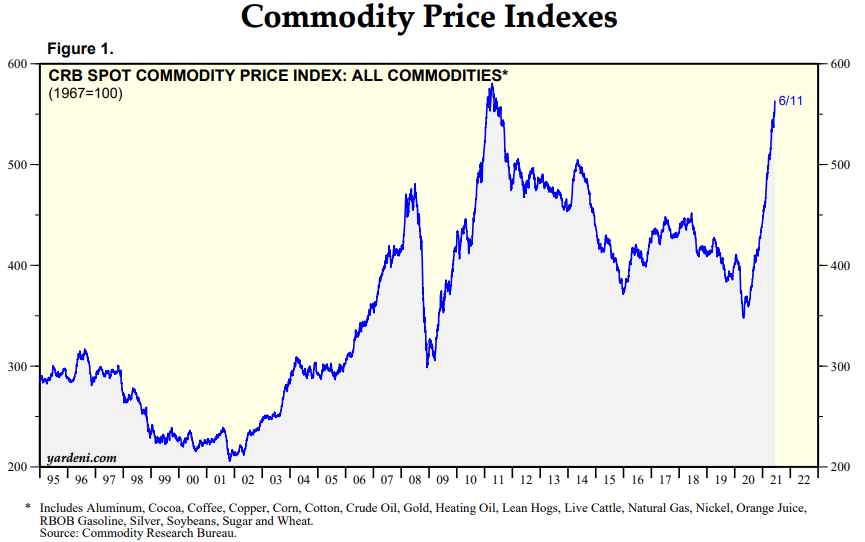

The chart beneath reveals the CRB index since 1995:-

Supply: CRB, Yardeni

This chart appears very totally different from the energy-heavy GSCI index, which is weighted on the idea of liquidity and by the respective world manufacturing volumes of its underlying elements: –

Supply: S&P GSCI, Buying and selling Economics

The small restoration on the chart above shouldn’t be that insignificant, nevertheless it represents a 55% improve because the lows of 2020. The truth that costs collapsed when the pandemic broke and subsequently skyrocketed when vaccines allowed economies to reopen , is hardly shocking. Financial cycles have a powerful affect on commodity costs; short-term, inelastic provide, confronted with an sudden soar in demand, invariably triggers sharp value will increase.

The shutdown that adopted the primary outbreak of the virus led to an abrupt change in shopper demand; lodges and journey had been out, telecommuting was in. Whereas home costs had been already supported by a pointy rate of interest reduce and debt reduction measures, the value of timber for dwelling enhancements and property extensions exploded: –

Supply: Commerce economic system

Comparable patterns had been evident in metal and copper, but additionally because of shortages and bottlenecks within the semiconductor provide chain, which led to a slowdown in automobile manufacturing, which in flip led to a rise within the value of each new and used automobiles.

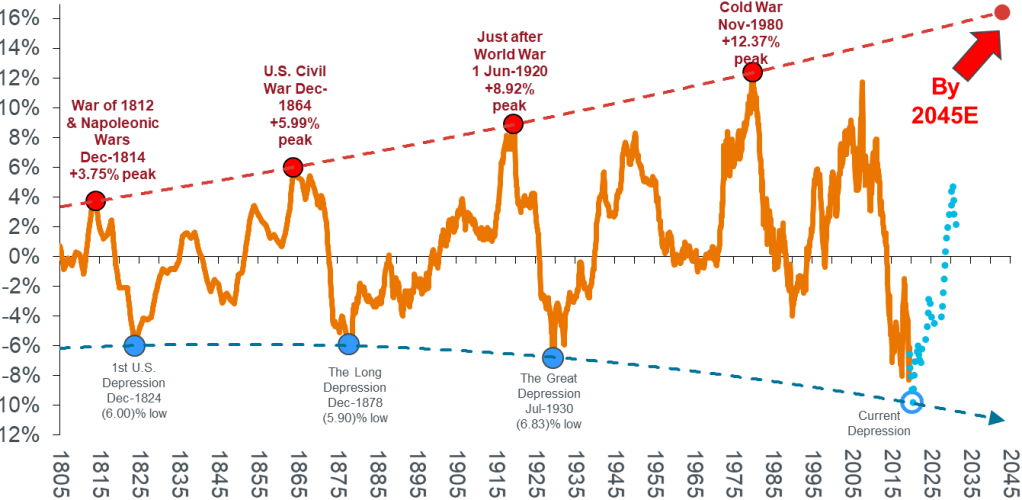

The latest resurgence in commodity costs has inspired recommendations {that a} new commodity supercycle is underway, however these are comparatively uncommon occasions. The newest cycle is mostly believed to have begun with the rise in Chinese language demand within the late Nineteen Nineties and ended abruptly with the monetary disaster of 2008/2009. For the reason that disaster, Chinese language progress has slowed, though India’s rise might even see one other wave of speedy industrialization in some unspecified time in the future. Nonetheless, the chart beneath depicts a special narrative, suggesting that the 2008 peak was only a corrective wave from the 1980 peak. The brand new tremendous cycle is simply starting, it can peak someday round 2045: –

Supply: Janus Henderson, Stifel report June 2020. Notice: Proven as 10-year rolling compound progress charge with polynomial development at prime and backside. Blue dashed line illustrates a forecast estimate. Warren & Pearson Commodity Index (1795-1912), WPI Commodities (1913-1925), equal weighted (1/3 ea.) PPI Power, PPI Farm Merchandise and PPI Metals (ferrous and non-ferrous) ex-precious metals ( 1926- 1956), Refinitiv Equal Weight (CCI) Index (1956-1994) and Refinitiv Core Commodity CRB Index (1994 to current).

One other near-term issue that has exacerbated the rise within the value of key commodities over the previous yr is the persevering with commerce tensions between the US and China. Tariff will increase have elevated prices for importers and wholesalers, whereas the impact of the Nice Monetary Disaster has been evident over the previous decade within the shortening of worldwide provide chains. Covid accelerated this deglobalization and compelled many corporations to hunt out new sources of provide. The long-term influence of those variations will probably be stronger, deeper provide chains, however the short-term prices should be paid by the importer, producer or shopper.

A part of the brand new commodity supercycle argument relies on extra structural components. The discount of carbon emissions will contain using large quantities of metals. Electrification requires copper; silver will probably be wanted for photovoltaic panels; Electrical automobiles require aluminium, nickel, graphite, cobalt and lithium, together with quite a few uncommon earth metals – of which China is quick changing into a monopoly provider.

The final main structural vitality shift was from coal to grease. Colonel Drake’s discovery in Pennsylvania in 1859 and the Spindletop discovery in Texas in 1901 set the stage for the brand new oil economic system, but it took till 1919 for gross sales of gasoline to exceed gross sales of kerosene.

Though coal-gas was used for many of the nineteenthth century, and the primary US pure fuel pipeline was in-built 1891, earlier than the Nineteen Twenties, the overwhelming majority of pure fuel produced as a byproduct of oil extraction was merely flared away. Superior welding strategies within the interwar years marked a growth within the introduction of pure fuel, however massive pipelines had been nonetheless below development as late because the Nineteen Sixties.

The timeline from Colonel Drake in 1859 to an enormous introduction of pure fuel took greater than a century. Expertise and innovation are shifting at a a lot sooner tempo at the moment, but the infrastructure funding required to rework from carbon to renewables will take a long time slightly than years.

In the meantime, there are nonetheless short-term causes to doubt the arrival of a brand new commodity supercycle so quickly on the final one. China’s GDP progress has fallen sharply from the double-digit charges of the previous decade. The working-age inhabitants is declining, and the Individuals’s Financial institution of China seems reluctant to permit credit score expansions on the dimensions of earlier cycles. Rebalancing in the direction of home consumption stays official coverage.

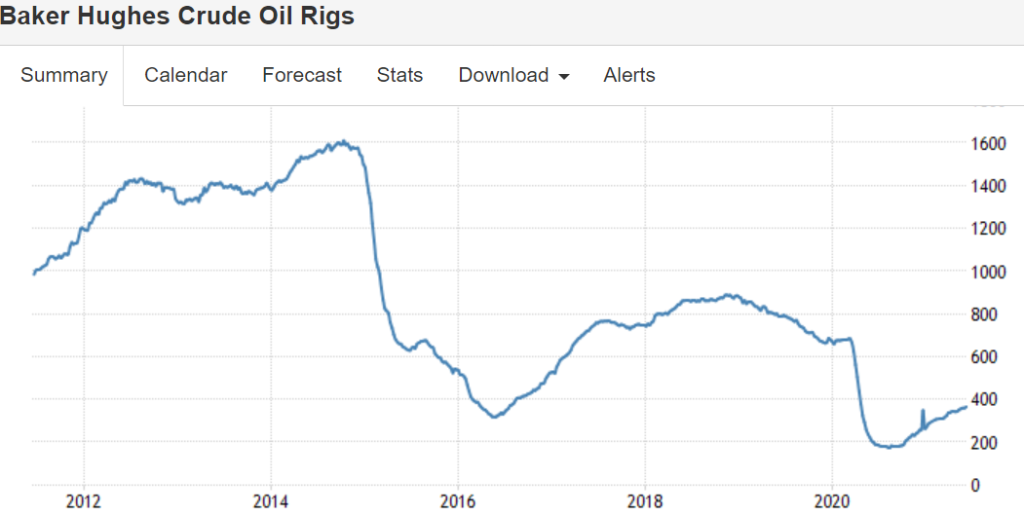

There may be short-term proof of vitality provide constraints, however in the long run, oil and fuel manufacturing, notably from US frackers, can improve manufacturing quickly in response to will increase within the value of crude oil. The chart beneath reveals the fluctuations within the variety of Baker Hughes US oil rigs over the previous decade, no scarcity of capability is obvious right here:-

Supply: Baker Hughes, Buying and selling Economics

Agricultural commodities are inclined to function on even shorter provide cycles. If provide constraints ship wheat costs increased, farmers reply by switching away from corn. Seasonal changes might be fast.

The GSCI could have hit its lowest because the Nineteen Eighties final April, and costs could have doubled since then, nevertheless it’s nonetheless greater than 75% beneath its June 2008 peak. Additional upside might be seen as the worldwide economic system recovers for a yr with misplaced financial progress, however as financial progress returns to regular, vitality demand is more likely to average simply as contemporary provide kicks in.

The US administration’s spending plans could maintain US demand, however China seems decided to nip its home credit score bubble within the bud. Broadly talking, these components counteract one another. In accordance with the Federal Reserve, US GDP is predicted to be between 5% and seven.3% in 2021, falling to 2.5% to 4.4% in 2022 and 1.7% to 2.6% in 2023, whereas Chinese language progress in response to OECD will decline. from 8.5% in 2021 to five.8% in 2022.

Conclusion and funding alternatives

Again in January, Goldman Sachs predicted a brand new commodity supercycle. They see rising wages resulting in sooner, optimistic commodity costs, housing formation and extra synchronized social insurance policies, much like these of the Nineteen Sixties ‘Warfare on Poverty’ marketing campaign. In different respects, they consider this cycle has stronger parallels to the Seventies than the 2000s. Goldman expects industrial funding to run at 2000 ranges, whereas social reconstruction generates a Seventies-style shopper growth.

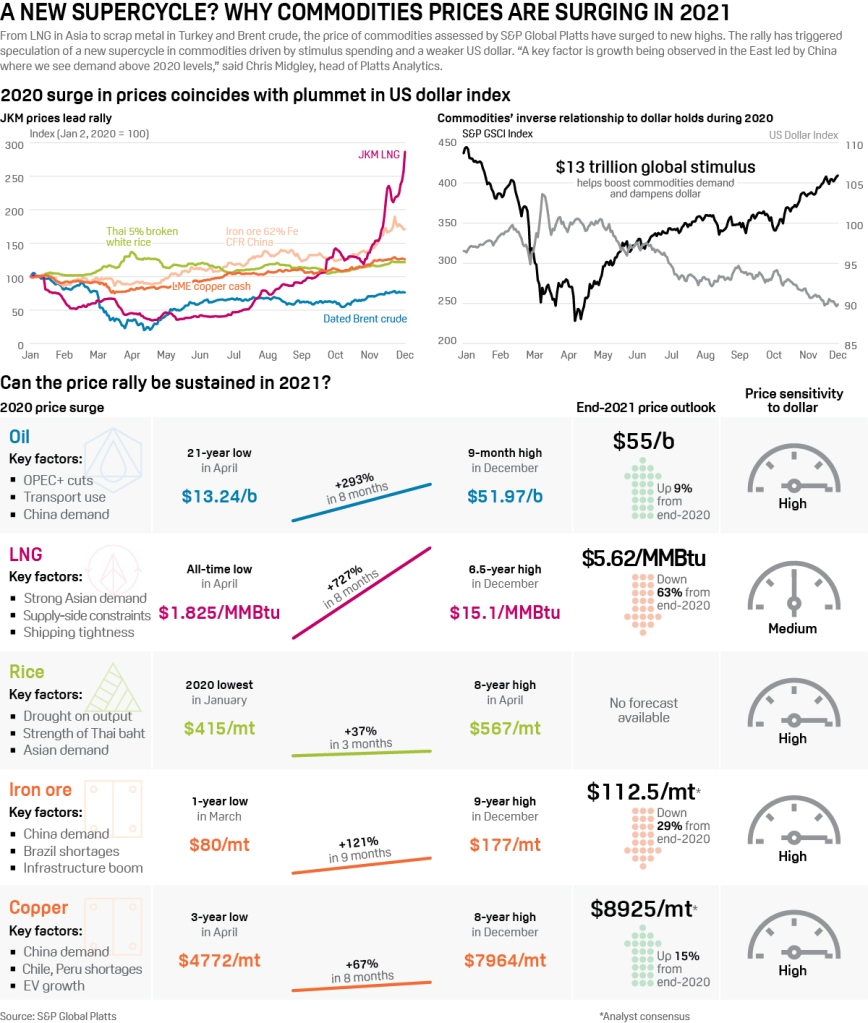

S&P presents a few of these arguments in a helpful infographic:-

Supply: S&P World

US unemployment has fallen from 11.1% to five.8% over the previous 12 months, even within the harder-hit eurozone it has fallen from 8.7% to eight%, whereas Chinese language knowledge has adopted an identical trajectory, down from 6.1% to five% since February 2020. Nonetheless, a lot of the worldwide economic system stays in a type of lockdown, with financial exercise pushed by fiscal spending. It’s nonetheless troublesome to think about the circumstances for a short-term sustainable financial growth. Take away international financial and financial easing and commodity demand will evaporate.

As a basic rule, in commodity and monetary markets, what goes up in value should finally come down once more. The worth of US Stud Lumber (chart above) is way from the highs. Governments and their central banks can attempt to take away the punch bowl, however the markets are unlikely to take it nicely.